Are you thinking about franchising? Dive into the latest franchise statistics;

Whether you’re starting out or expanding, it’s crucial to understand the current trends. Franchising is a booming industry, worth nearly $900 billion globally in 2024. But there’s a lot more to learn. From the U.S. to international markets.

Let’s explore the latest franchise statistics and see what the future holds.

Franchise Statistics (Editor’s Pick)

- There are over 773,000 franchises in the United States alone, employing over 8.4 million people.

- Franchise output is projected to increase by 4.1% from its 2023 value of $858.5 billion, reaching $893.9 billion in 2024.

- New franchises have a success rate that is 6.3% higher than that of independent companies after one year.

- In 2023, roughly 8.66 million workers were employed by U.S. franchise establishments.

- The global franchise market is projected to grow by $1.63 trillion between 2022 and 2027, with an annual growth rate of 9.58%.

- 70% of franchises have invested in digital marketing, and 60% have implemented online ordering and delivery systems.

- 80% of franchisees aim to increase revenue, and 70% aim to expand their business.

- 80% of franchisees struggle to find and retain top talent, and 70% offer competitive salaries and benefits to attract employees.

- 70% of franchisees value ongoing support from their franchisor, and 60% expect regular communication and training.

General Franchise Statistics

- The global franchise market is projected to expand by $1.63 trillion between 2022 and 2027, with an annual growth rate of 9.58%. (Source)

- The average franchise owner is 44 years old. (Source)

- Food-related franchises make up 37% of the total, while the remaining franchises are distributed across 28 other sectors. (Source)

- Most franchise owners are White (67.2%), followed by Hispanic or Latino (15.4%), Asian (6.4%), and Black or African American (6.2%). (Source)

- New franchises have a success rate that is 6.3% higher than that of independent companies after one year. (Source)

- In 2024, the business services sector is forecast to see a 1.8% increase in franchise locations, growing to 104,000 establishments. This growth will lead to an additional 32,000 jobs and a 3.8% increase in industry output, contributing $107.6 billion to the economy. (Source)

- As of 2023, approximately 806,270 franchise establishments were operating in the United States. (Source)

- A substantial 86% of franchise owners reported experiencing the negative effects of rising costs on their businesses, although this figure is slightly lower than the previous year’s. (Source)

- Franchise output is anticipated to increase by 4.1% from its 2023 value of $858.5 billion, reaching $893.9 billion in 2024. (Source)

- The GDP of franchises is forecast to continue its upward trajectory, growing by 4.3% to $545.8 billion in 2024. (Source)

- There are over 3,000 distinct franchise brands available. (Source)

- According to FRANdata, there were approximately 774,965 franchise establishments in 2021, with a growth rate of 2.8%, exceeding the historical average for most years. (Source)

- The total number of franchised establishments is projected to increase by 1.9% to 822,000 units. (Source)

- The franchise retail output sector is projected to increase by 3.1% in 2024, adding $4.1 billion to the industry. Additionally, franchise retail establishments are expected to grow by 3,500 units, creating over 40,000 new jobs. (Source)

- The lodging industry is forecast to experience modest growth in 2024, with a 0.9% increase in franchises to 36,000, a 4.5% rise in output to $97.2 billion, and a corresponding boost in employment to 723,000 jobs. (Source)

- McDonald’s generated $15.4 billion in revenue from its franchised restaurants worldwide in 2023. The majority of this revenue, $9.84 billion, came from rent, while $5.53 billion was derived from royalties. (Source)

- The real estate, healthcare, residential, business services, automotive, and retail sectors collectively account for more than half of the franchise industry. (Source)

- The commercial and residential services sector is anticipated to grow in 2024. The number of franchise businesses in this sector will increase by 2%, reaching a total of 81,000. Jobs will also rise by 2%, to 315,000. (Source)

- The sector’s output is expected to grow by 4.6%, valued at $59.8 billion, driven by a recovering housing market. (Source)

- Franchise locations experienced a 2.6% decline in 2020. (Source)

Franchise Workforce Data (Franchise Statistics)

- U.S. business services franchise employment experienced steady growth from 2013 to 2019, reaching 650,000. However, it declined to 588,000 in 2020 due to the pandemic and slowly recovered in 2023, adding an additional 34,000 jobs. (Source)

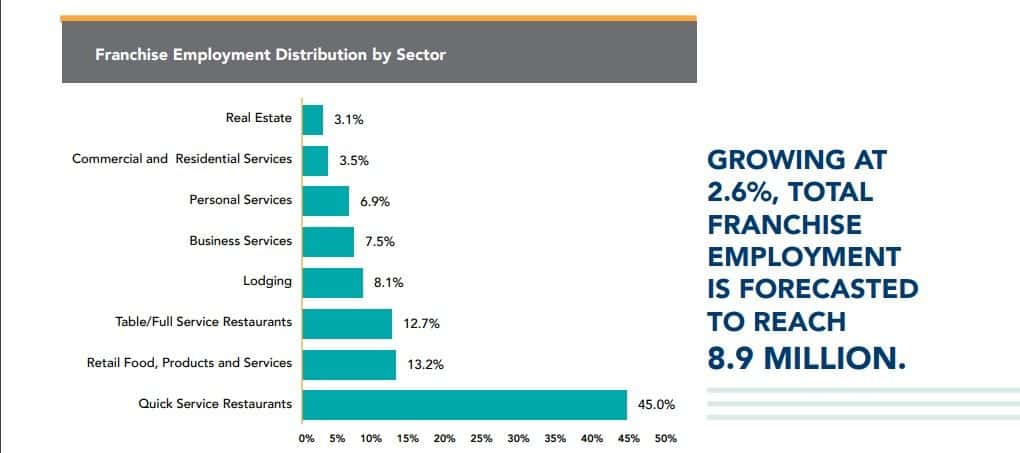

- Franchise employment is projected to grow by 2.6%, adding over 221,000 jobs to a total of 8.9 million employees. This is a slight decrease from the 244,000 jobs added in 2023. Service-based industries, such as business and personal services, are expected to drive employment growth in 2024, with a projected growth rate of 5.1%. (Source)

- Franchise businesses employ over 8.2 million Americans, and in 2021, franchises contributed nearly USD 788 billion to the economy. (Source)

- The full-service restaurant sector was projected to see a 2.5% increase in franchise locations in 2022, reaching 32,819 establishments and supporting a workforce of approximately 1.1 million employees. (Source)

- The IFA estimated that franchise employment would increase by 8.8% in 2021 to 8.2 million, a net gain of 660,300 jobs from 2020. (Source)

- Employment in franchising is projected to increase by 2.6% in 2024 to a total of 8,886,555 employees in the U.S. (Source)

- Franchises create 2.3 times more jobs than non-franchise businesses of similar size. Furthermore, franchises generate 1.8 times more taxable revenue than independent businesses. (Source)

- Employees of franchise businesses earn up to 3.4% more and have better access to health insurance (65%) and paid leave (76%). (Source)

- The U.S. Census Bureau reports that franchise businesses recently made up over 11% of all businesses with paid employees across 295 industries. (Source)

- A significant 80% of respondents indicated struggling with staffing shortages, with unfilled job vacancies impacting their franchises. (Source)

- In 2023, U.S. franchise establishments employed roughly 8.66 million workers. (Source)

- According to ADP’s National Franchise Report, the U.S. gained an average of 46,400 franchise jobs per month in 2021. (Source)

- Franchise employment declined by 11.2% to 7.5 million in 2020, losing approximately 940,000 jobs due to limited capacity and revenue deterioration. (Source)

- In 2022, 85% of U.S. franchised businesses increased employee wages, and 60% planned to continue this trend in 2023. Additionally, 43% of franchises enhanced employee benefits in 2022, with 42% intending to do the same in 2023. (Source)

- Labor costs and quality remain a primary challenge for 34% of franchise businesses, down from 47% in 2023. (Source)

U.S. Franchise Data (Franchise Statistics)

- There are over 712,274 franchise owners employed in the U.S. at present. (Source)

- The U.S. commercial and residential services franchise industry remained unaffected by the pandemic, exhibiting steady output growth since 2013, reaching $57 billion in 2023. (Source)

- The U.S. business services franchise industry recovered to pre-pandemic levels in 2023, generating $104 billion. The industry grew 30% from 2013 to 2019, peaking at $106 billion, but declined to $91.3 billion in 2020 due to the pandemic. (Source)

- The food industry was disproportionately impacted by inflation, with three of the top five industries most affected being food-related. (Source)

- McDonald’s outpaced all other U.S. franchises in global sales in 2022, reaching $118 billion, compared to 7-Eleven’s $93.5 billion. (Source)

- In 2019, over half (54%) of all franchised businesses in the U.S. were owned by multi-unit franchise operators. (Source)

- According to the International Franchise Association, the franchise industry experienced substantial growth in 2021, opening over 21,000 new locations and creating more than 660,000 additional employment opportunities across the United States. (Source)

- The Southeast region leads the nation in franchised businesses, accounting for 30% of the total U.S. franchised businesses, employing 2.6 million people, and generating a staggering $268.2 billion in revenue. (Source)

- The Southeast region is projected to see a 3.5% increase in franchise establishments, while the Southwest region is anticipated to experience a 3% growth. (Source)

- In 2023, there were approximately 195,507 fast-food franchise locations in the U.S., encompassing various types of quick-service eateries, including burger joints, pizza places, and sandwich shops. (Source)

- Over 50 million Americans consume fast food daily. That represents 37% of the population. (Source)

- The personal services franchise industry rebounded to pre-pandemic levels in 2023, generating $42 billion, and is projected to reach $46 billion in 2024. After steady growth from 2013 to 2019, the industry suffered a 33% decline in 2020 due to the pandemic, dropping to $26 billion. (Source)

- Franchise businesses contributed US $670 billion to the U.S. economy in 2020, representing 3% of the total nominal GDP. (Source)

- 83% of voters in a survey have a favorable view of locally owned franchise small businesses in the United States. Additionally, more than half of voters (57%) use franchise businesses regularly. (Source)

- 64% of voters believe locally-owned businesses are more likely to support the local community. (Source)

- Nearly all (90%) franchise business units increased their prices to offset rising costs and maintain profitability. (Source)

- The initial investment to open a Kentucky Fried Chicken (KFC) franchise in the U.S. was approximately $3.7 million, with $1.9 million allocated for building and site costs and $100,000 for permits, licenses, and security deposits. (Source)

- The initial investment to open a Burger King franchise was approximately $4,520,900, with $1.6 million allocated for improvements and construction, and $50,000 for the franchise fee. (Source)

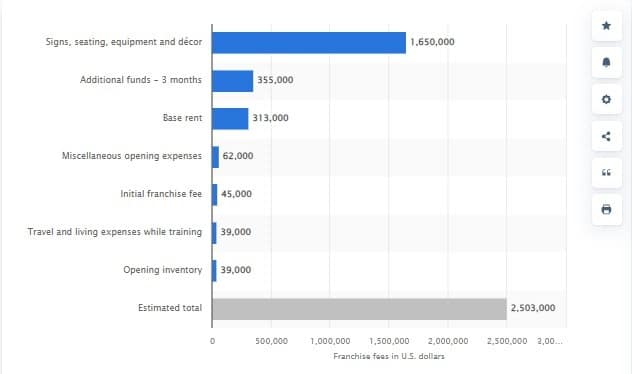

- The initial investment to open a McDonald’s franchise was estimated at $2,503,000, with $1,650,000 allocated for signs, seating, and decor. (Source)

- The franchise output was forecast to increase by 5% in 2022 to USD 76.4 billion. (Source)

- The initial investment to open a Taco Bell franchise in 2023 was estimated at $3.37 million, including $1.4 million for real property and $45,000 for the franchise fee. (Source)

- The initial investment to open a Dunkin’ Donuts franchise in 2023 was estimated at $1.81 million, not including real property. Building costs accounted for $600,000, and the franchise fee was $90,000. (Source)

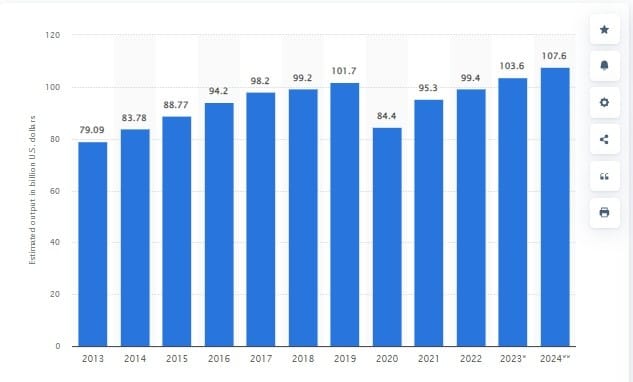

- In 2023, the economic output of franchise establishments was valued at approximately USD 859 billion. In 2020, the sector experienced losses due to the COVID-19 pandemic, with an estimated economic output of approximately USD 677 billion, compared to USD 794 billion in 2019. (Source)

- One in twelve Americans in the private sector works in a franchise business or has a job because of franchising. (Source)

- One nickel of every dollar of economic output in the private sector is attributable to franchising. (Source)

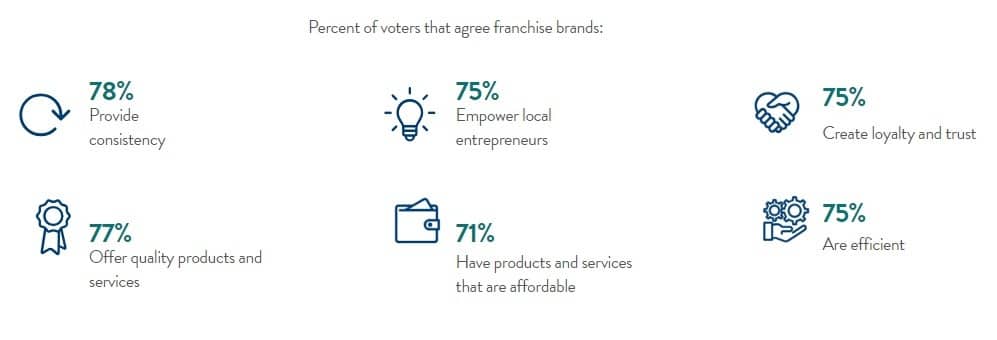

- A survey found that 78% of voters believe franchise brands offer a consistent experience. (Source)

- A survey found that 75% of voters believe franchise brands empower local entrepreneurs. (Source)

- The same survey states that 75% of voters agreed that franchises create trust and loyalty. (Source)

- Franchise market growth in the Southeast and Southwest will outpace other regions in the U.S. in 2024, as the top 10 states for franchise growth are Texas, Florida, Georgia, North Carolina, South Carolina, Tennessee, Maryland, Arizona, Colorado, and Virginia. In contrast, California and Washington are expected to see a decline in franchise growth, dropping by 4.2% and 2.3%, respectively. (Source)

- The proportion of U.S. businesses operating as franchises declined by 9.4% between 2014 and 2020, with some metropolitan areas experiencing declines as high as 63.5%. (Source)

Franchise Data for Other Regions (Franchise Statistics)

Canada

- Canada’s franchising GDP expanded from $100 billion in 2019 to $120 billion in 2024. As the 12th largest sector in the country and the second largest globally, Canada’s franchise industry contributes significantly to the nation’s economy. (Source)

- Canada’s franchise industry ranks second globally, following only the United States. (Source)

- In Canada, there are approximately 76,000 franchised outlets operated by between 1,200 and 1,300 franchise companies. (Source)

- Ontario dominates the Canadian franchising landscape, with 56% of franchise companies headquartered there, primarily in the Greater Toronto Area, and 65% of all franchise outlets operating within the province. (Source)

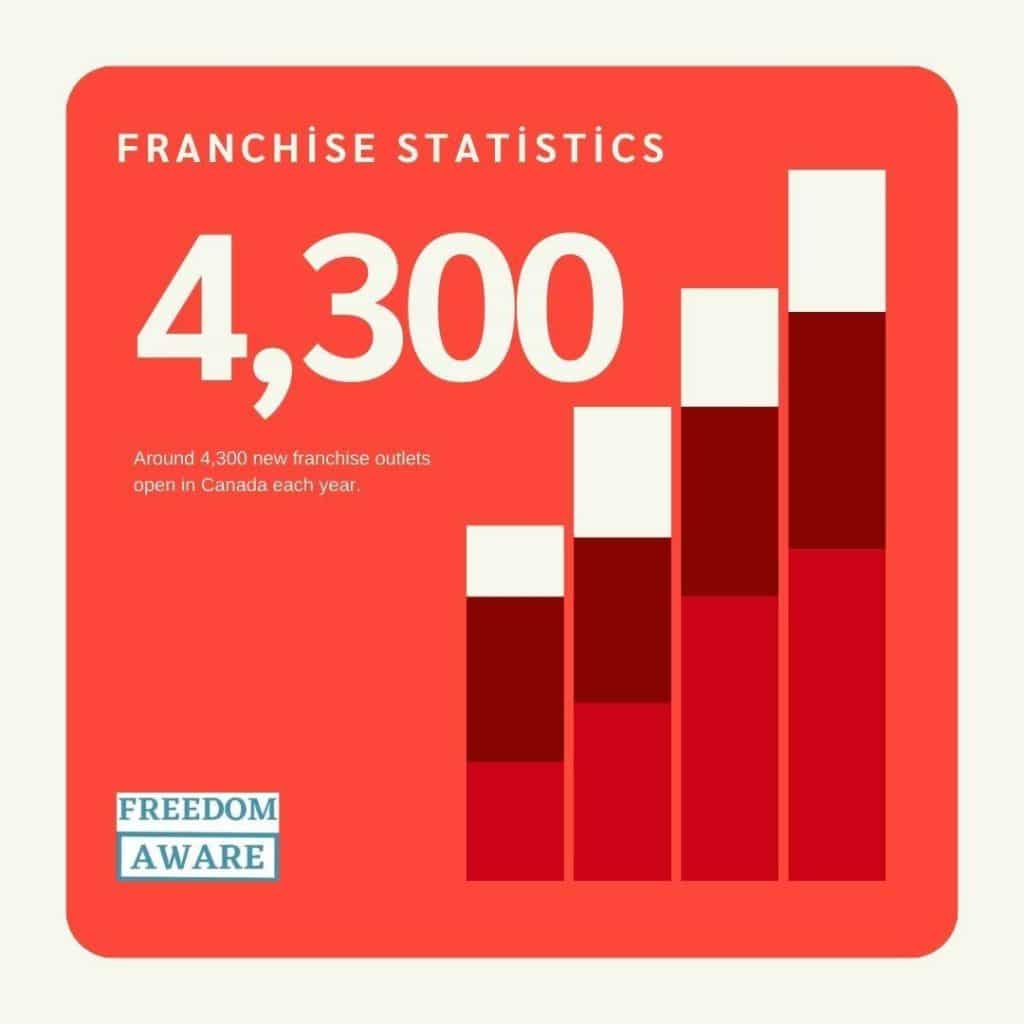

- Around 4,300 new franchise outlets open in Canada each year. (Source)

- Franchising employs over 1.5 million Canadians, representing one in every ten workers in the country. (Source)

Australia

- Market share concentration in the Australian franchising industry is low, with the top four companies accounting for 32% of market revenue in 2024. (Source)

- Australia’s franchise sector plays a significant role in the country’s economy, with 95% of franchisors and almost all franchisees being small businesses with fewer than 20 employees. (Source)

- The non-food retail sector is the most sought-after for franchising in Australia, comprising over 25% of all franchise systems. (Source)

- Australia boasts 1,344 franchise systems with approximately 98,000 units, generating $184 billion in revenue and employing over 598,000 people. (Source)

- 60% of franchisors in Australia have been involved in franchising for over 10 years. (Source)

- 92% of franchise systems in Australia are locally owned and operated, with the majority being homegrown Australian businesses that have been franchising for an average of nine years. (Source)

- 28% of Australian franchise systems have expanded to international levels. (Source)

- Lockdowns, trading restrictions, and social distancing measures since March 2020 have presented numerous challenges for franchised businesses in Australia. (Source)

- The Franchise Council of Australia represents the country’s franchise industry, which comprises over 1,200 franchise networks, more than 94,000 individual outlets, and employs over 565,500 people, contributing a significant $174 billion to the national economy. (Source)

- In Australia, almost 300 franchise systems have a history of over 20 years, and 30% of franchisees have been involved for 5-10 years, with 40% having been in business for over 10 years. (Source)

- Women play a substantial role in Australia’s franchise industry, owning approximately 34% of franchises and holding numerous leadership positions, contributing significantly to the economy with an annual value of $6 million. (Source)

- In Australia, women-owned franchises drive growth, outperforming the overall sector with an impressive 7.8% average annual growth rate, significantly higher than the industry average. (Source)

- Australia’s franchise industry contracted to $185.1 billion in 2024, experiencing a 2.4% annual decline over 5 years. (Source)

- Franchised businesses in Australia are heavily concentrated in New South Wales, Victoria, and Queensland. (Source)

Africa

- Franchising in South Africa generated an estimated R999 billion in turnover for 2023. This represents a 36% increase from 2019, accounting for 15% of South Africa’s GDP. (Source)

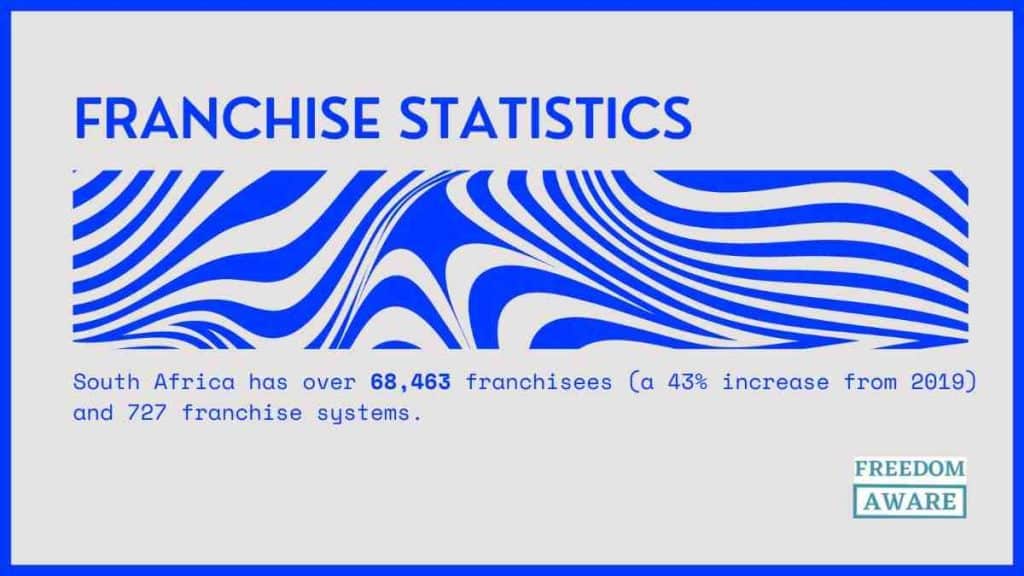

- South Africa has over 68,463 franchisees (a 43% increase from 2019) and 727 franchise systems. (Source)

- Based on volume, fast-food and Quick Service Restaurant operators are the top franchises in Nigeria, accounting for 45% of the franchises. (Source)

- The franchising finance market in Africa is valued at $93.9 billion, with available funding amounting to $37.6 billion, resulting in a financing gap of $7.51 billion. (Source)

Others

- UK fast-food franchise industry revenue is projected to grow from £12.1 billion to £12.7 billion by 2024-25, with a 3.8% increase in the final year. (Source)

- France boasts over 1,965 franchise networks, 79,134 sales locations, 795,441 employees, and a total turnover of €68.8 billion. (Source)

- China boasts over 4,000 franchise brands and 500,000 franchise outlets. (Source)

- The typical initial investment for a franchise in Singapore ranges from S$30,000 to S$150,000. (Source)

- South Korea has the highest number of franchise brands, with over 4,800 concepts. India closely follows in second place, with nearly 3,922 franchise systems. Taiwan ranks third, boasting over 3,300 franchise brands. (Source)

- In 2021, South Korea’s franchise sector employed 834,290 individuals, with 186,776 working in convenience stores. (Source)

- South Korea’s franchise industry grew by 10.6% in 2021, with 259,662 stores driven partly by increased demand for foreign food. The combined revenue of franchise stores rose by 14.2% to 84.8 trillion won (or USD 66.5 billion). (Source)

- As a subsidiary of Yum! Brands, KFC expanded its global footprint to 29.9 thousand restaurants in 2023, an increase from the prior year’s 27.7 thousand. (Source)

Conclusion (Franchise Statistics)

The franchise industry is a dynamic and growing sector, offering entrepreneurs and investors a proven business model and support to succeed. By understanding the latest franchise statistics and trends, you can make informed decisions and stay ahead of the competition. Whether you’re considering investing in a franchise or looking to expand your existing business through franchising, these statistics provide valuable insights into the state of the industry.